Do you know the current market value of your home? With our TrueValueIndex®, you’ll know as soon as you open up your DomiDocs profile. But for an insurance company, they’ll probably require more information to confirm the value by conducting an in-person 4-point inspection of your home. Let’s find out the details of what you can expect during a 4-Point inspection.

Do you know the current market value of your home? With our TrueValueIndex®, you’ll know as soon as you open up your DomiDocs profile. But for an insurance company, they’ll probably require more information to confirm the value by conducting an in-person 4-point inspection of your home. Let’s find out the details of what you can expect during a 4-Point inspection.

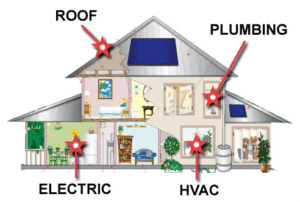

What is a 4-Point Inspection?

Insurance companies and underwriters use a 4-point inspection as a tool to determine risk within your home. This examination by a building contractor or licensed inspector will include 4 areas of your home to determine they’ve all been maintained and are in good working order. What they’re looking for:

- Electrical – the overall condition and type of wiring used throughout your home, as well as the manufacturer and the electrical panel itself

- Heating/ventilation/air conditioning (HVAC) – is there a central heating/air conditioning system? How old is it? Are there any signs of leaks?

- Plumbing – the type of pipes used throughout the home, along with the age of the hot water tank and any signs of possible leakage

- Roof/structure – What type of roof material do you have? How old is the roof and what’s the general condition? Are there signs of water damage or any missing tiles?

The examiner will fill out a detailed form for each of the 4 areas and will also take photos to provide to the insurance company.

Why is a 4-Point Inspection Needed?

In many cases, a 4-point inspection is required simply because of the age of your home. As a rule of thumb, if your home is 40 years old or above, most insurance companies will require a detailed 4-point inspection. If you have a newer home, chances are you won’t need to have this done at all.

If I’ve Had a Full Home Inspection Already, Can I Use This Instead of a 4-Point Inspection?

According to insurance experts in Florida, even if you’ve already had a full inspection of your home, you really shouldn’t volunteer any extra information to an insurance company than you have to. Sometimes a full report will include unnecessary details such as cosmetic or minor damage that won’t reflect well overall, so if you’re asked to only provide a 4-point inspection, do so.

What Does a 4-Point Inspection Cost & Who Conducts It?

On average, a 4-point inspection will run in the neighborhood of $50-100. If you’re not sure who to hire, consult the DomiDocs list of nationwide trusted service providers. Generally, if you’re switching insurance companies, you can use an already conducted 4-point inspection as long as it’s no more than 2 years old.